QUICK ANSWER

The hardest Florida real estate exam questions usually test Florida-specific application, not obscure trivia. For 2026 candidates, the highest-risk patterns are escrow timing, brokerage relationship duties, sales associate compensation, documentary stamps, mortgage taxes, tenancy by the entireties, homestead protection, EXCEPT and NOT wording, proration setup, and score-report remediation after a failed attempt.

PRACTICE QUESTION SCOPE ONLY

This guide uses original practice questions and explanations. It does not copy, reconstruct, or claim to reveal Pearson VUE exam questions. The goal is to train the Florida rules and calculation patterns behind difficult questions so you can reason through new scenarios on test day.

Some Florida real estate exam questions feel hard because the correct answer is the Florida answer, not the national textbook answer. A generic rule like "handle escrow promptly" will not save you when the question asks for the sales associate deadline and the broker escrow deadline. A memorized rate will not save you if you apply the deed rate to the note. A contract definition will not save you if the stem quietly says EXCEPT.

The official Florida Department of Business and Professional Regulation (DBPR) sales associate candidate information booklet describes a closed-book 100-question exam with a 3.5-hour time limit, 19 content areas, and a passing score of 75 points or higher. The exam is built around Florida real estate principles, Florida law, and math. That is why the best way to prepare for hard questions is not to hunt for leaked questions. It is to learn the recurring Florida traps that make otherwise fair questions feel difficult.

The 10 hardest Florida question patterns

Snippet answer: The hardest Florida real estate exam questions usually come from scenario-based Florida law and math. Expect difficult stems around escrow timing, transaction broker duties, sales associate compensation, deed and note taxes, intangible tax, tenancy by the entireties, homestead, EXCEPT/NOT wording, proration, and how to study after a failed attempt.

| Hard pattern | Why candidates miss it | Florida anchor |

|---|---|---|

| Escrow timing | They merge the associate handoff and broker deposit deadlines | F.S. 475.25, F.A.C. 61J2-14.008, F.A.C. 61J2-14.009 |

| Brokerage relationships | They confuse transaction broker duties with single-agent fiduciary duties | F.S. 475.278 |

| Sales associate compensation | They think later broker notice cures a direct payment problem | F.S. 475.42 |

| Documentary stamps | They swap the deed rate and the note rate | F.S. 201.02, F.S. 201.08 |

| Mortgage tax and refinancing | They tax the full new loan when only the increase matters in the setup | F.S. 199.133, F.S. 201.08 |

| Tenancy by the entireties | They confuse it with tenancy in common or ordinary joint tenancy | F.S. 689.115 and Florida ownership principles |

| Homestead protection | They assume a dollar cap instead of Florida acreage and exception rules | Florida Constitution Article X, Section 4 |

| EXCEPT and NOT wording | They answer the true statement instead of the false one | Exam strategy |

| Proration | They use the wrong day count or charge the wrong party | Florida closing math |

| Retake study decisions | They study broadly instead of using result-report detail and diagnostics | DBPR/Pearson VUE score-report process |

PRACTICE THE HARD PATTERNS

Use Florida-specific questions, not generic real estate drills.

Pass Florida is an educational exam-prep tool for Florida sales associate candidates: 1,002 Florida-specific practice questions, a 19-topic diagnostic mapped to the DBPR outline, six modes, Math Coach across the 14 Florida math calculation types, Trap Library, Confidence Calibration, offline app access on phone or tablet, optional sync, lifetime updates, and one $39.99 purchase. No subscription. No copied exam questions.

Why these questions feel harder than normal

Snippet answer: Florida exam questions feel hard for four reasons: a Florida-only rule, a timing deadline, two similar numbers, or stem wording like EXCEPT that changes the logic.

Florida hard questions usually have one of four problems hiding inside the stem.

First, the question uses a Florida-only rule. Tenancy by the entireties, Florida brokerage relationship disclosures, documentary stamp tax, and Florida homestead protection do not behave like generic national examples.

Second, the question asks for timing. Escrow deadlines, complaint timelines, exam scheduling windows, renewal timing, and post-license deadlines punish vague memory.

Third, the question uses two similar numbers. Deed stamps and note stamps look similar. Intangible tax and note tax both involve mortgage documents. Proration can use a 365-day year, a 360-day banker year, or a 30-day-month setup depending on the stem.

Fourth, the question changes the logic. EXCEPT, NOT, LEAST likely, BEST, and FIRST all change what the answer choice must do.

EXAM TIP

When a Florida question feels hard, pause before calculating. Ask: is this testing a Florida statute, a Florida Real Estate Commission (FREC) rule, a math convention, or the wording of the stem? Most misses happen before the first calculation.

Practice Questions 1-3: Florida Law Traps

Snippet answer: These three questions test the Florida law traps candidates miss most: the separate escrow deadlines, transaction broker confidentiality, and sales associate compensation through the employer broker.

Use these as study questions, not as memorization targets. The real exam can ask the same rule with different names, dates, numbers, and distractors.

Question 1: escrow timing

A Florida sales associate receives a buyer's earnest money deposit on Monday. The sales associate gives it to the broker on Wednesday morning. The broker deposits it into the escrow account on Friday. Which statement is best?

A. The associate and broker both acted on time.

B. The associate acted late, but the broker deposited the funds on time.

C. The associate acted on time, but the broker deposited the funds late.

D. Both the associate and broker acted late.

Answer: D. Both acted late. The sales associate must deliver the deposit to the broker by the end of the next business day after receipt, so a Monday receipt makes Tuesday the deadline and Wednesday is late. For the broker, receipt by the sales associate counts as receipt by the broker, so the broker's three-business-day deposit clock also starts Monday: Tuesday, Wednesday, Thursday. Placing the funds on Friday is the fourth business day, which is late. The associate's delay does not extend the broker's deposit deadline.

Why it is hard: Many candidates memorize one deadline and apply it to both people, or they assume the broker's clock restarts when the broker physically receives the check. Florida measures the broker's deposit deadline from the sales associate's receipt, because receipt by the associate is receipt by the broker.

Study link: Review the full escrow breakdown in Florida real estate escrow trust account rules.

Question 2: transaction broker duties

A Florida licensee is working as a transaction broker in a residential sale. The buyer says, "Do not tell the seller I would pay more than this offer." Which answer best describes the licensee's duty?

A. The licensee must disclose it because transaction brokers owe full disclosure.

B. The licensee may keep that information confidential unless waived in writing.

C. The licensee must become a single agent before writing the offer.

D. The licensee may not work with both parties in Florida.

Answer: B. Florida transaction brokers provide limited representation. F.S. 475.278 includes limited confidentiality, unless waived in writing by a party. That includes information such as the buyer being willing to pay more than the submitted offer.

Why it is hard: Candidates often mix up single-agent duties, transaction broker duties, and no-brokerage duties. Florida also presumes transaction brokerage unless single agency or no brokerage relationship is established in writing.

Study link: Use Florida real estate brokerage relationships explained for the full duty comparison.

Question 3: sales associate compensation

A buyer gives a Florida sales associate a $1,000 thank-you payment after closing. The sales associate immediately tells the broker and asks whether the broker is okay with it. Which answer is best?

A. It is allowed because the sales associate disclosed it to the broker.

B. It is allowed because the payment came after closing.

C. It is a problem because sales associate money in a brokerage transaction must be handled in the employer's name and with the employer's express consent.

D. It is allowed if the buyer signs a receipt.

Answer: C. F.S. 475.42 says a sales associate may not collect money in connection with a real estate brokerage transaction, including commission, deposit, payment, rental, or otherwise, except in the name of the employer and with the employer's express consent. The statute also limits commission or compensation actions to the registered employer.

Why it is hard: Disclosure helps in some compliance contexts, but it does not rewrite the sales associate's compensation structure. The exam may test whether you understand who controls brokerage compensation.

Practice Questions 4-6: Tax and Ownership Traps

Snippet answer: These questions test the right rate on the right document, the taxable base on a refinance, and survivorship under tenancy by the entireties.

Question 4: documentary stamps on deed and note

A Florida property sells for $420,000. The buyer obtains a $330,000 mortgage note. Using the standard statewide exam rate, what are the documentary stamps on the deed and note?

A. Deed $1,470; note $2,940

B. Deed $2,940; note $1,155

C. Deed $2,310; note $2,940

D. Deed $1,155; note $2,940

Answer: B. Deed documentary stamps use $0.70 per $100 of consideration: $420,000 / $100 = 4,200; 4,200 x $0.70 = $2,940. Note documentary stamps use $0.35 per $100: $330,000 / $100 = 3,300; 3,300 x $0.35 = $1,155.

Why it is hard: The trap is not arithmetic. The trap is applying the correct rate to the correct document.

EXAM TIP

Write D = deed = 70 and N = note = 35 before you calculate. If the stem mentions Miami-Dade or a surtax, follow the stem. If it does not, use the standard statewide setup used in most practice math.

Study links: Drill the rates in Florida real estate exam documentary stamps and closing costs and run numbers in the documentary stamp tax calculator.

Question 5: mortgage tax and refinancing

A borrower refinances a Florida mortgage. The old mortgage balance was $250,000 and the new mortgage is $310,000. The question asks for the nonrecurring intangible tax on the increase only. What amount should be taxed?

A. $60,000

B. $250,000

C. $310,000

D. $560,000

Answer: A. The setup asks for the increase only: $310,000 minus $250,000 equals $60,000. Florida's nonrecurring intangible tax is imposed at 2 mills on obligations secured by Florida real property. In many refinance questions, the key move is identifying whether the question taxes the new amount or only the increase.

Why it is hard: Candidates see a new mortgage number and jump straight to multiplying. The stem controls the taxable base.

Question 6: tenancy by the entireties

A married couple takes title to Florida real property as tenants by the entireties. One spouse dies. Which statement is best?

A. The deceased spouse's interest passes through probate under the will.

B. The surviving spouse receives title by survivorship.

C. The property converts into tenancy in common with the heirs.

D. The state receives the deceased spouse's interest.

Answer: B. Tenancy by the entireties is a Florida ownership form associated with married couples and survivorship. When one spouse dies, the surviving spouse receives the interest by operation of law.

Why it is hard: Candidates confuse tenancy by the entireties with tenancy in common. Tenancy in common has no automatic survivorship. Tenancy by the entireties is built around the marital unit.

SEE THE TRAP, THEN DRILL IT

Reading one trap is not the same as recognizing the next one.

Pass Florida puts these exact patterns in front of you until the Florida answer becomes automatic: 1,002 Florida-specific questions, a Trap Library, Math Coach, and a 19-topic diagnostic, for one $39.99 purchase. No subscription. No copied exam questions.

Practice Questions 7-10: Wording and Math Traps

Snippet answer: These questions test the transaction broker presumption, EXCEPT and NOT wording, constitutional homestead protection, and a 360-day proration setup.

Question 7: brokerage relationship presumption

A Florida residential buyer meets a licensee at a showing. The buyer has not signed a single-agent agreement, and no no-brokerage relationship has been established in writing. Which relationship is presumed?

A. Single agent

B. Transaction broker

C. Dual agent

D. No brokerage relationship

Answer: B. F.S. 475.278 presumes transaction brokerage unless a single-agent relationship or no brokerage relationship is established in writing. Florida does not allow a licensee to operate as a disclosed or nondisclosed dual agent.

Why it is hard: Many candidates remember the three relationship names but miss the default rule. The exam can ask the default in a short fact pattern where nothing has been signed.

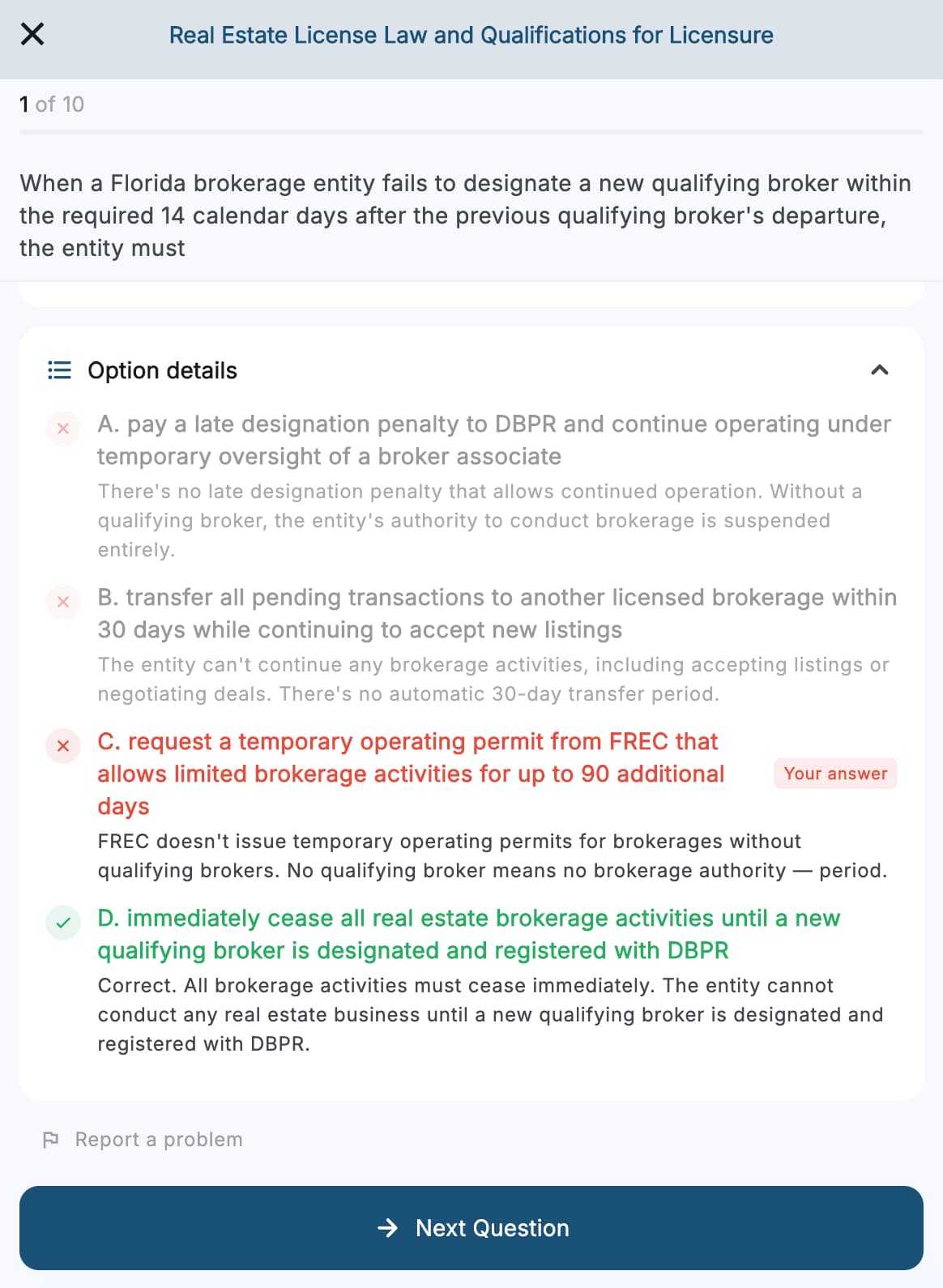

Question 8: EXCEPT and NOT wording

A question asks: "All of the following are duties of a Florida transaction broker EXCEPT." Which method gives you the best chance of avoiding the trap?

A. Pick the answer choice that sounds most familiar.

B. Look for the false statement after testing each option as true or false.

C. Ignore the word EXCEPT because it is only a formatting convention.

D. Pick the longest answer because it is usually more complete.

Answer: B. EXCEPT means the exam is asking for the choice that does not belong. Treat each answer as true or false, cross out the true statements, and choose the false one.

Why it is hard: Under time pressure, candidates answer the topic instead of the question. The word EXCEPT changes the logic.

Study link: Practice the format in EXCEPT and NOT questions on the Florida real estate exam.

Question 9: homestead protection

A Florida homeowner's primary residence is protected as homestead. A judgment creditor from an unrelated personal loan wants to force a sale of the residence. Which statement is best under Florida's constitutional homestead protection?

A. The creditor can force sale for any judgment.

B. The creditor can force sale only above a fixed dollar cap.

C. Homestead generally protects the residence from forced sale, subject to specific exceptions such as taxes, purchase or improvement obligations, and certain labor obligations on the realty.

D. Homestead protection applies only to renters.

Answer: C. Florida Constitution Article X, Section 4 protects qualifying homestead property from forced sale under process of any court, subject to listed exceptions. It uses acreage limits rather than a general dollar cap: one-half acre inside a municipality or 160 acres outside a municipality.

Why it is hard: Candidates from other states often expect a dollar cap. Florida homestead protection is different, and the exceptions matter.

Study link: Review the exam version in Florida real estate exam homestead exemption.

Question 10: proration with a 360-day year

Annual taxes are $3,600. The question says to use a 360-day year and prorate through the day before closing. Closing is September 15. What is the seller's share?

A. $2,540

B. $2,580

C. $2,610

D. $3,600

Answer: A. With a 360-day year, each month has 30 days. January through August equals 8 months x 30 = 240 days. The seller is charged through September 14, which adds 14 days. Total seller days = 254. Daily rate = $3,600 / 360 = $10. Seller share = 254 x $10 = $2,540.

Why it is hard: The math is simple after the setup. The miss usually comes from using 365 days, including the closing day when the question says day before closing, or failing to convert months to 30 days.

Study links: Work more examples in Florida real estate exam proration, then drill formulas in Florida real estate exam math formulas.

Topic-weighted study order for hard questions

Snippet answer: Two weeks out, study hard patterns by DBPR weight: contracts and relationships first, then property rights and titles, then mortgages and tax math, then license law and FREC discipline.

The DBPR outline matters because not all difficult topics carry the same practical study value. A candidate who is two weeks from test day should study hard patterns in this order.

| Priority | Study area | Why it deserves attention |

|---|---|---|

| 1 | Contracts, brokerage activities, and authorized relationships | Each is heavily tested and turns on scenario language |

| 2 | Property rights, titles, deeds, and legal descriptions | Many questions are concept traps rather than memory checks |

| 3 | Residential mortgages, closing computations, and taxes | The numbers are predictable, but the setup changes |

| 4 | License law, violations, and FREC discipline | Statute wording controls the answer |

| 5 | Appraisal, planning, zoning, and investment topics | Usually manageable if you know the formulas and definitions |

Do not spend all your time on the scariest-looking math. Florida math is finite. It is better to master the 14 math calculation types, then use the rest of your study time on Florida law scenarios.

What these hard questions have in common

Snippet answer: In hard Florida questions, the wrong answer is usually a true statement placed in the wrong context, so the best habit is explaining why each distractor is wrong.

The hard questions share a pattern: the wrong answer is usually a true statement in the wrong context.

A buyer's willingness to pay more is confidential in a transaction broker setup, but a single agent has different duties. A $0.70 rate is real, but it belongs to the deed, not the note. A 365-day year may be reasonable in life, but the question may instruct you to use a 360-day banker year. Homestead protection is broad, but it still has listed exceptions.

That is why the best study habit is to explain why the wrong answer is wrong. If you can only name the right answer, you may be memorizing. If you can explain the distractor, you are much closer to exam readiness.

How to study these in the next 20 minutes

Snippet answer: In 20 minutes, label each missed question by rule type, reread the official rule, do five mixed questions, then write one trap sentence naming what you confused.

Minutes 1 to 5: mark the rule type. For each missed question, label it as Florida statute, FREC rule, math convention, or question wording.

Minutes 6 to 10: reread the rule, not your notes. Use the official source when possible. For brokerage relationships, read F.S. 475.278. For compensation, read F.S. 475.42. For deed and note taxes, compare F.S. 201.02 and F.S. 201.08.

Minutes 11 to 15: do five mixed questions. Avoid drilling only the topic you just studied. The real exam is mixed, so your practice should force switching.

Minutes 16 to 20: write one trap sentence. After a miss, write: "I missed this because I confused ___ with ___." That sentence is your next review target.

Ready to Practice the Hard Patterns

The best next step is to face these patterns under pressure: sit a free timed practice exam and see how the hard traps behave when the clock is running.

Prefer to warm up first? Drill the headline traps with authorized relationships practice and violations and penalties practice, use Math Drill for the calculations, or download Pass Florida for the full Florida-specific question bank on your phone.

Frequently Asked Questions

What are the hardest questions on the Florida real estate exam?

The hardest Florida real estate exam questions usually involve Florida-specific law and scenario wording. Common hard patterns include escrow timing, brokerage relationships, direct sales associate compensation, documentary stamps, intangible tax, tenancy by the entireties, homestead protection, EXCEPT/NOT wording, proration math, and remediation after a failed attempt.

Does Pearson VUE publish the hardest Florida real estate exam questions?

No. Pearson VUE and DBPR do not publish the live exam question bank. Good practice material should use original Florida-specific questions that test the same rules and reasoning skills without copying or reconstructing live exam questions.

Are Florida real estate exam questions tricky?

The questions are usually fair, but they can feel tricky because distractors sound familiar. The exam often tests whether you can apply a Florida rule in a scenario, not whether you recognize a definition in isolation.

Which Florida real estate exam math questions are hardest?

The hardest math questions usually involve documentary stamps, note tax, intangible tax, proration, loan-to-value, discount points, commission, and area or acreage conversions. The formulas are learnable, but the stem decides which formula applies.

How many hard questions can I miss and still pass?

The sales associate exam is scored on 100 points, and 75 points or higher is passing. Since DBPR says all questions are equally weighted, you have room to miss some hard questions. The safer goal is not perfection. It is reducing preventable misses in Florida-specific law and setup-based math.

Should I memorize Florida statute numbers for the exam?

You do not need to memorize statute numbers as answer choices. You should know the rules well enough to recognize the scenario. Statute numbers are useful for studying because they lead you back to the official source when a prep explanation feels too general.

Why do I get hard questions wrong even after studying for weeks?

Many candidates study definitions for weeks but practice too few scenario questions. A definition-only habit can fail when the exam asks who gets the money, what deadline applies, what disclosure is required, or which party receives a debit or credit.

What should I do if I failed because of hard questions?

Use your score, exam-review notes, and Florida-specific practice diagnostics to find the pattern. Do not restart from page one. Build a retake plan around the weakest official content areas and the question formats you misread. Our Florida real estate exam score report study plan explains that process.

Is the Florida real estate exam mostly national or Florida-specific?

The exam includes general real estate concepts, but DBPR's outline ties the sales associate exam to Florida law, Florida rules, and Florida practice. Candidates who rely on national-only prep usually feel the gap most in brokerage relationships, escrow, taxes, homestead, and Florida-specific ownership rules.

What is the fastest way to improve on hard Florida questions?

Practice mixed Florida questions with explanations, then review the official rule behind each miss. After that, redo a similar question with different numbers or facts. That trains recognition instead of memorizing one answer.

Methodology and source notes

How this guide was built. This post was reviewed against the Pass Florida content signoff checklist on June 20, 2026. It prioritizes Florida-only accuracy, official-source alignment, original practice questions, clear disclosures, search-intent coverage, internal links, and human-readable explanations. It avoids out-of-state rules, generic national shortcuts, copied exam questions, and unsupported pass guarantees.

Official exam source. DBPR's Florida real estate sales associate candidate information booklet, effective January 2025, describes the exam as closed book with 100 multiple-choice questions, a 3.5-hour time limit, a passing score of 75 points or higher, and 19 content areas based on Florida real estate principles, Florida law, and math.

Statute and rule verification. This article was verified against the currently published 2025 Florida Statutes pages available in June 2026, including F.S. 475.25, F.S. 475.278, F.S. 475.42, F.S. 201.02, F.S. 201.08, F.S. 199.133, F.S. 689.115, and Florida Constitution Article X, Section 4. Escrow timing references should be verified directly against F.A.C. 61J2-14.008 and F.A.C. 61J2-14.009 before using them for real-world compliance.

Product note. Pass Florida is our Florida-specific exam-prep app, so the relationship is direct and disclosed. It is an educational exam-prep tool for Florida sales associate candidates: 1,002 Florida-specific practice questions, a 19-topic diagnostic mapped to the DBPR outline, six modes, Math Coach across the 14 Florida math calculation types, Trap Library, Confidence Calibration, offline app access on phone or tablet, optional sync, lifetime updates, and one $39.99 purchase. No subscription. No copied exam questions. Pass Florida is independent exam preparation, not a DBPR-approved pre-licensing course, a tutoring service, a Pearson VUE scheduling tool, a licensing-activation service, legal advice, tax advice, brokerage advice, or a guarantee of passage.

Sources

- DBPR Florida real estate sales associate candidate information booklet

- F.S. 475.25, discipline and escrow-related trust obligations

- F.S. 475.278, authorized brokerage relationships

- F.S. 475.42, sales associate violations and compensation limits

- F.S. 201.02, documentary stamps on deeds

- F.S. 201.08, documentary stamps on notes and mortgage documents

- F.S. 199.133, nonrecurring intangible tax

- F.S. 689.115, estate by the entirety in mortgages made or assigned to spouses

- Florida Constitution Article X, Section 4, homestead protections

- Florida Administrative Code Chapter 61J2, FREC rules

- F.A.C. 61J2-14.008, escrow definitions

- F.A.C. 61J2-14.009, sales associate deposit delivery

This post is exam-prep coaching content for Florida real estate sales associate candidates. It is not legal, tax, financial, lending, appraisal, brokerage, insurance, title, closing, licensing, compliance, or professional advice. Florida statutes, FREC rules, DBPR materials, Pearson VUE procedures, exam specifications, and pass-rate context can change. The examples and patterns are original educational explanations, not copied or reconstructed Pearson VUE exam questions. Verify current rules with official sources or qualified professionals for real-world decisions. Studying with Pass Florida or any other exam-prep tool does not guarantee passage of the state exam.